Advertisement

Advertisement

Column-Funds start 2023 short dollars, eyeing U.S. rate peak: McGeever

By:

By Jamie McGeever ORLANDO, Fla. (Reuters) - Hedge funds have started 2023 betting that U.S. interest rates are close to peaking, that the Federal Reserve will keep them higher for longer and that the dollar will weaken slightly.

By Jamie McGeever

ORLANDO, Fla. (Reuters) – Hedge funds have started 2023 betting that U.S. interest rates are close to peaking, that the Federal Reserve will keep them higher for longer and that the dollar will weaken slightly.

Judging by the economic data, financial market swings and talk from U.S. policymakers in the first week of the year, this would appear to be a reasonable – and reasonably consensus – macro strategy to employ.

At least for now.

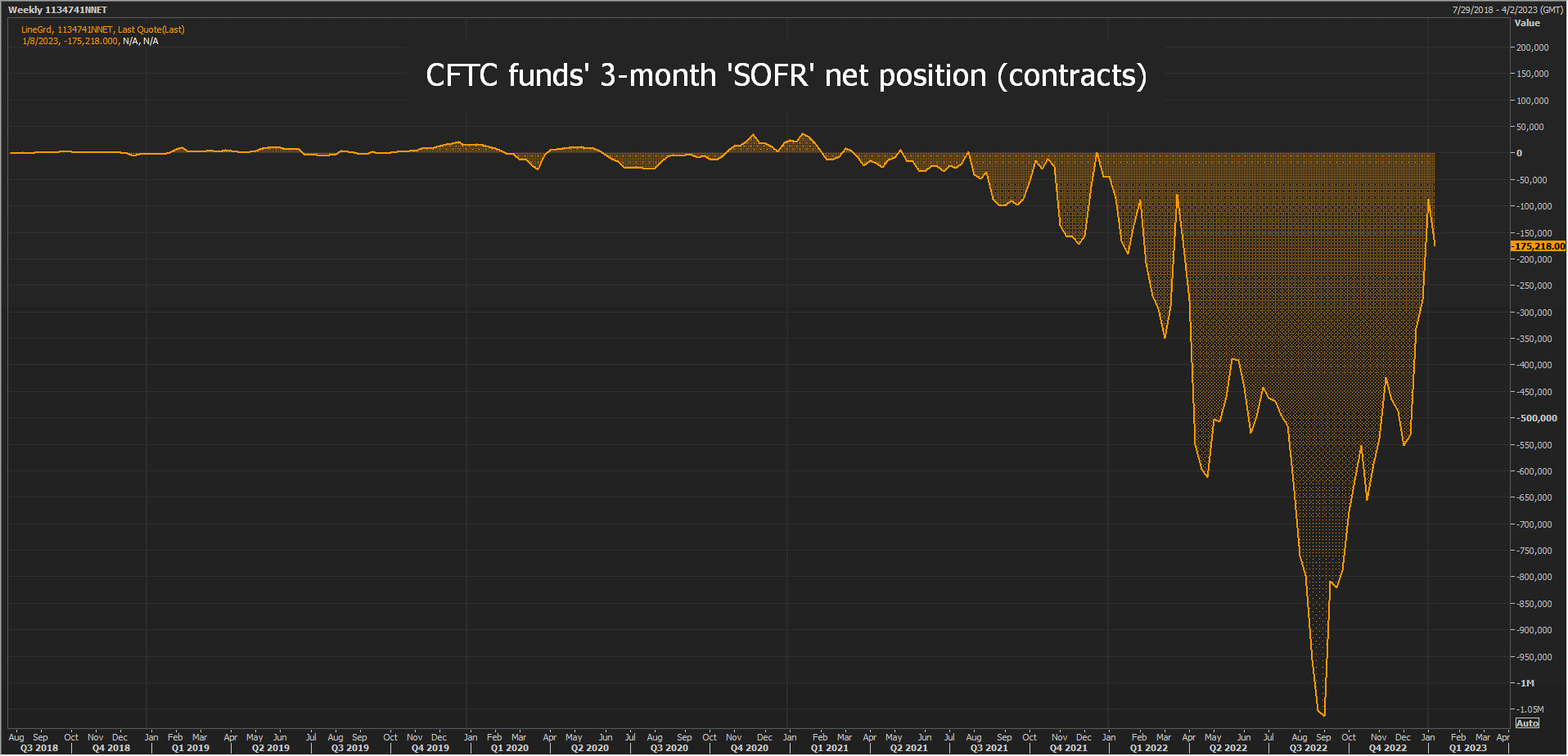

Commodity Futures Trading Commission (CFTC) data show that speculators closed 2022 with one of the smallest three-month SOFR rate futures short positions of the year, a light short dollar position, and substantial short positions cross the U.S. Treasuries curve.

A short position is essentially a wager that an asset’s price will fall, and a long position is a bet it will rise. In bonds and interest rates, yields and implied rates fall when prices rise, and move up when prices fall.

CFTC speculators increased their net short position in three-month Secured Overnight Financing Rate (SOFR) futures to 175,218 contracts in the week through January 3, but that is still one of the smallest net short positions of a tumultuous year.

Funds’ U.S. interest rate expectations reached fever pitch around August and September last year when their net short position exceeded 1 million contracts.

The rapid reversal since then shows they are much more neutral on the rate and inflation outlooks this year and think the Fed is close to ending its hiking cycle, or they have taken profit on a highly lucrative trade. Or both.

“The bottom line is that the Fed and the consensus are right to expect a decline in inflation as we go through 2023,” reckons Torsten Slok, partner at Apollo Global Management in New York.

Bond capitulation looming?

Hedge funds are on track for their worst returns in 14 years in 2022, but macro strategies have performed much better. Industry data provider HFR’s macro index was up 8.15% in the first 11 months of the year, and the currency index was up 12.58%.

HFR is expected to release its December and full-year 2022 returns figures this week, and industry peer Preqin will follow later in the month.

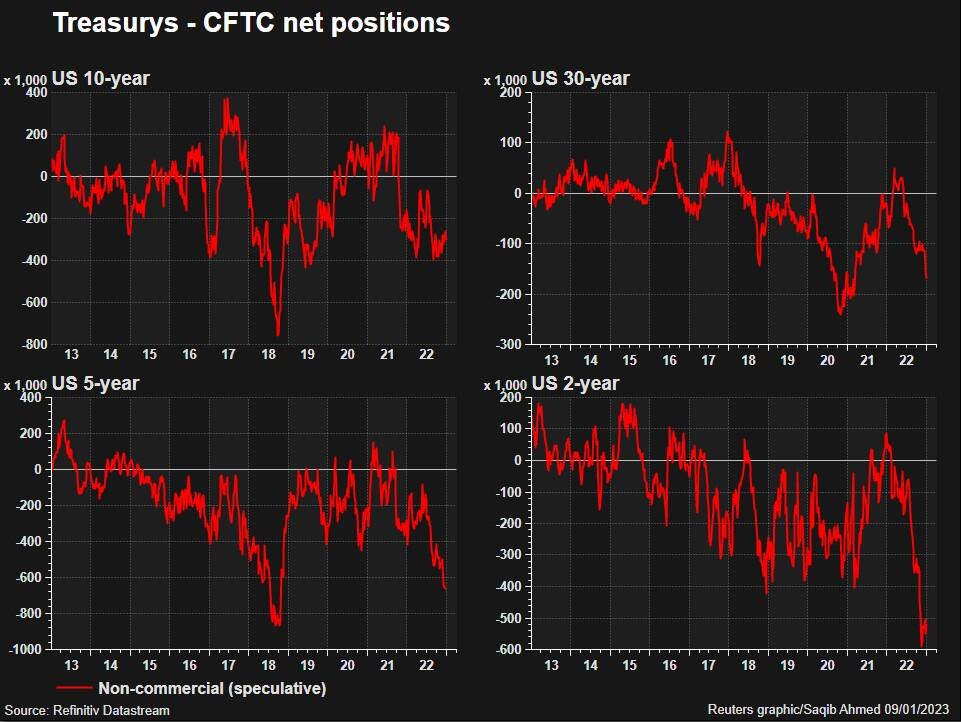

CFTC speculators’ small wager on short-term U.S. rates stands in contrast to the substantial bets they still retain against two- and 10-year Treasuries, even though the end of the Fed’s hiking cycle and economic slowdown are both coming into view.

In the 10-year space, funds ended 2022 with their third largest net short position of the year, at 383,602 contracts. Funds have been short these futures since October 2021, and the selling bias has strengthened recently – pullbacks have been quickly followed by weeks of even larger bearish bets.

Since hitting a 15-year high of 4.30% in October the 10-year yield has fallen; it closed at 3.57% on Friday. The yield curve inversion deepened in that time too, meaning the 10-year yield fell further below the two-year.

But funds have retained their substantial net short position. If this is the year to buy bonds because they are cheap – outright and relative to equities – funds may be forced to U-turn.

Funds trimmed their net short exposure to two-year Treasury futures in the week through Jan. 3 – but only slightly – to 521,508 contracts, still one of the largest ever.

Funds have been short two-year futures all year and any notion of positioning for a Fed pivot was dashed in October when they ramped up their bearish bets to record levels.

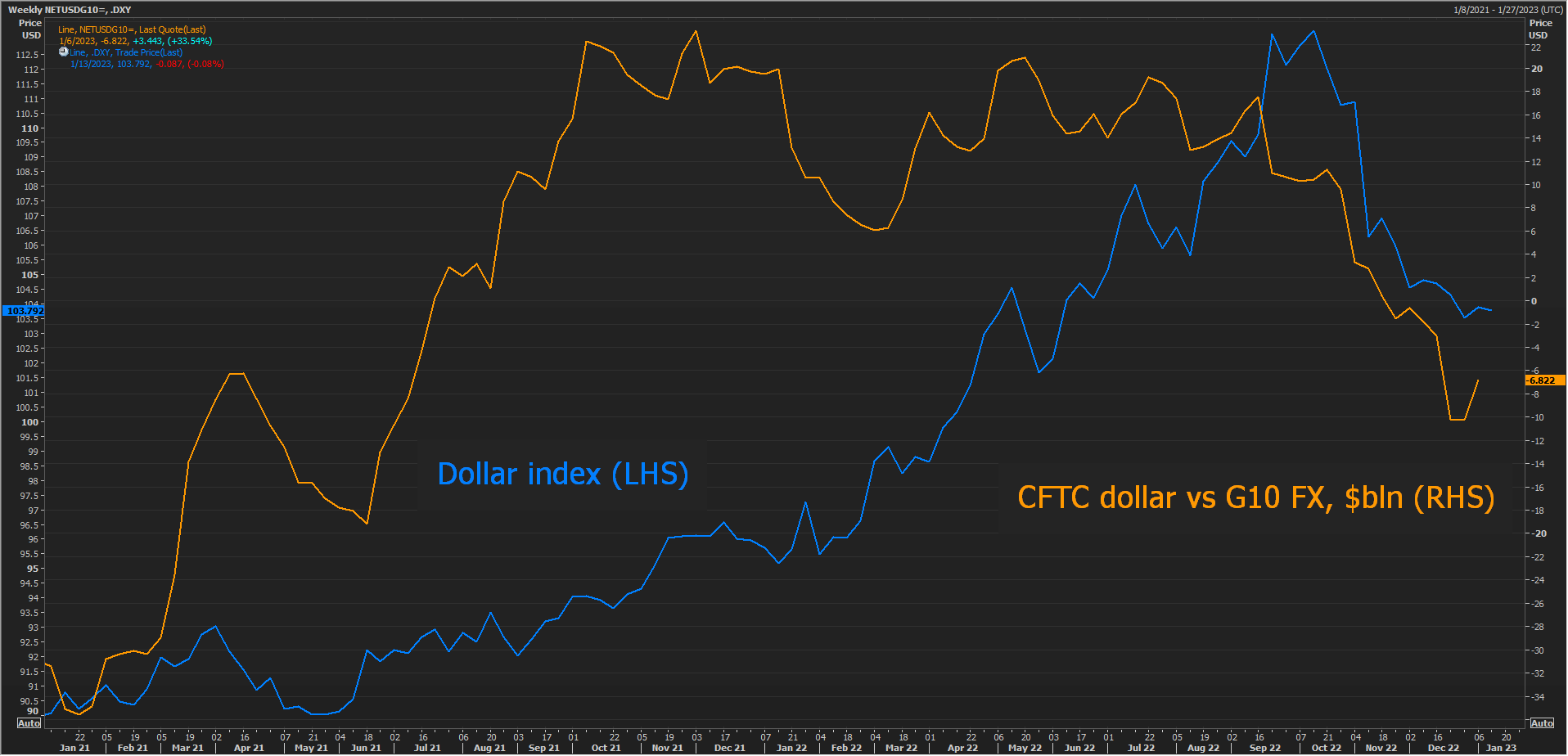

In foreign exchange, funds reduced their net short dollar position by around a third, closing the year with a $6.8 billion bet that the dollar would weaken against its G10 currency peers.

That is driven by the sizeable long euro position. Funds’ bet on the euro appreciating against the dollar – close to the biggest in two years – is worth $17 billion and overwhelms the $4.5 billion and $1.5 billion long-dollar bets against the yen and sterling, respectively.

(The opinions expressed here are those of the author, a columnist for Reuters.)

(By Jamie McGeever; Editing by Bradley Perrett)

About the Author

Reuterscontributor

Reuters, the news and media division of Thomson Reuters, is the world’s largest international multimedia news provider reaching more than one billion people every day. Reuters provides trusted business, financial, national, and international news to professionals via Thomson Reuters desktops, the world's media organizations, and directly to consumers at Reuters.com and via Reuters TV. Learn more about Thomson Reuters products:

Did you find this article useful?

Latest news and analysis

Advertisement