Advertisement

Advertisement

$460M Worth of BTC Long Positions Liquidated in Past 24H as Market Drop Flushes Excess Leverage

Published: Jan 13, 2025, 14:55 GMT+00:00

Key Points:

- Over $460M in Bitcoin long positions were liquidated in the past 24 hours

- Market sentiment swings from extreme greed to neutral territory in just 30 days

- Technical indicators point to an impending crash for Bitcoin if the price drops below $95K

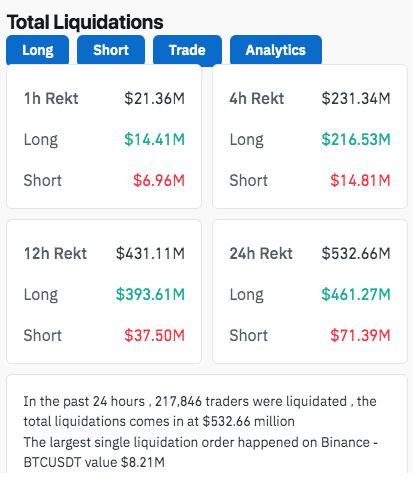

Bitcoin’s latest drop has wiped out $460 million worth of long positions in the past 24 hours as market participants seem to have gotten a bit too excited about the post-election rally.

Nearly half of that amount was flushed out of the market in the past 4 hours according to data from CoinGlass. In total, over 217,000 traders were liquidated as a result of the latest weakness that the price of Bitcoin (BTC) has experienced in the past day.

Last week’s strong jobs report in the United States may have contributed to accelerate Bitcoin’s pullback. On Friday, the Bureau of Labor Statistics reported that 256,000 new jobs were created in December, exceeding by a long-shot the consensus estimate of 155,000 new positions for the period.

The price of Bitcoin has been retreating since last Tuesday when it traded above $100,000 for the last time. Since then, the cryptocurrency has booked an 11.4% drop while it is trading 16.4% below its all-time high of $108,364.

Traders may have gotten ahead of themselves lately and were apparently expecting a comeback for Bitcoin in the near as indicated by this significant 24-hour liquidation.

Head and Shoulders Pattern Warns of Impending Bitcoin Crash

The latest drop in BTC’s price has pushed it near a psychological support area at $90,000 that bulls will likely defend with everything they got as a break below this threshold could result in the cryptocurrency moving back near its 200 simple moving average (SMA).

The chart above indicates that a head and shoulders pattern has been forming lately. This bearish setup would be confirmed if the price moves below $90,500. Although a retest is of that support area typically occur, a breakout of this nature could push BTC back to its 200 SMA in the next few months.

Meanwhile, trading volumes in the past 24 hours have more than doubled to $45.1 billion as per data from CoinMarketCap. In a scenario of significant price weakness, rising volumes are not good news as they indicate that traders are serious about their eagerness to sell.

The Feed and Greed Index for crypto is currently neutral but has been rapidly moving from 80 (extreme greed) back in mid-December to neutral territory at 47 as of today.

A History of Steep Corrections

Analyst Axel Bitbalze noted on his X account, which is followed by over 124,000 users, that post-halving drops like this are nothing new or different from what Bitcoin has experienced in the past.

Back in January 2017, BTC dropped from $1,185 to $800 and a similar retreat happened in January 2021 when the price of the cryptocurrency slid from $42,000 to $28,000. In both instances, the price recovered just a few weeks later and surged to fresh all-time highs.

A short-term decline would also not be entirely inconsistent with the state of the market as the Trump rally may have exhausted all of its ammo in November-December while the Federal Reserve’s actions at the end of this month are now in focus.

Last week’s strong jobs report favors a scenario where the U.S. central bank could temporarily halt a decision to lower interest rates as the economy is performing well without this kind of intervention.

As high-risk assets, cryptocurrencies benefitted from an increase in the market’s liquidity and loose financial conditions. Hence, the Fed’s inaction reduces the odds that Bitcoin can climb to a fresh all-time high in the near term in the absence of another bullish catalyst that can propel it to those levels.

About the Author

Alejandro Arriecheauthor

Alejandro Arrieche specializes in drafting news articles that incorporate technical analysis for traders and possesses in-depth knowledge of value investing and fundamental analysis

Did you find this article useful?

Latest news and analysis

Advertisement