Advertisement

Advertisement

Japanese Yen Weekly Forecast: Will USD/JPY Break 145 on December BoJ Rate Bets?

By:

Key Points:

- USD/JPY falls 3.23% to 149.707 as BoJ rate hike bets rise; key Japan data and US labor data could drive further volatility.

- Economists predict household spending to drop 2.6% YoY, potentially dampening demand-driven inflation in Japan.

- US labor data, including JOLTs and payrolls, may drive Fed rate expectations, influencing USD/JPY price levels.

USD/JPY Slides Below 150 on BoJ Rate Hike Bets

How far can the USD/JPY slide on market expectations for a December Bank of Japan rate cut?

Here’s What Traders Need to Know About

The USD/JPY pair tumbled by 3.23% to 149.707 in the week ending November 29. After climbing to 154.719, the pair slid to a low of 149.460 on November 29. Market speculation about a December Bank of Japan rate hike fueled Japanese Yen demand.

Manufacturing PMI in Focus

On Monday, December 2, the finalized Jibum Bank Manufacturing PMI needs consideration. The preliminary PMI slipped from 49.2 in October to 49.0 in November. A lower PMI may temper bets on a December BoJ rate hike. The manufacturing sector accounts for around 20% of Japan’s workforce and over 20% of Japan’s GDP.

A more marked contraction may affect the labor market, slowing wage growth and consumer spending. Weaker consumer spending could dampen demand-driven inflation.

Services PMI: A Key Indicator for BoJ Policy

On Wednesday, December 4, the finalized Jibun Bank Services PMI could be pivotal to a December BoJ rate hike. The preliminary PMI increased from 49.7 in October to 50.2 in November, signaling a return to expansion. An upward revision to the PMI may boost bets on a December rate hike. The services sector accounts for over 70% of Japan’s GDP and is pivotal in monetary policy decisions.

Beyond the headline figure, investors should consider price trends. Rising prices could fuel underlying inflation, supporting a BoJ rate hike. According to the Flash PMI survey, output prices accelerated while input price inflation softened.

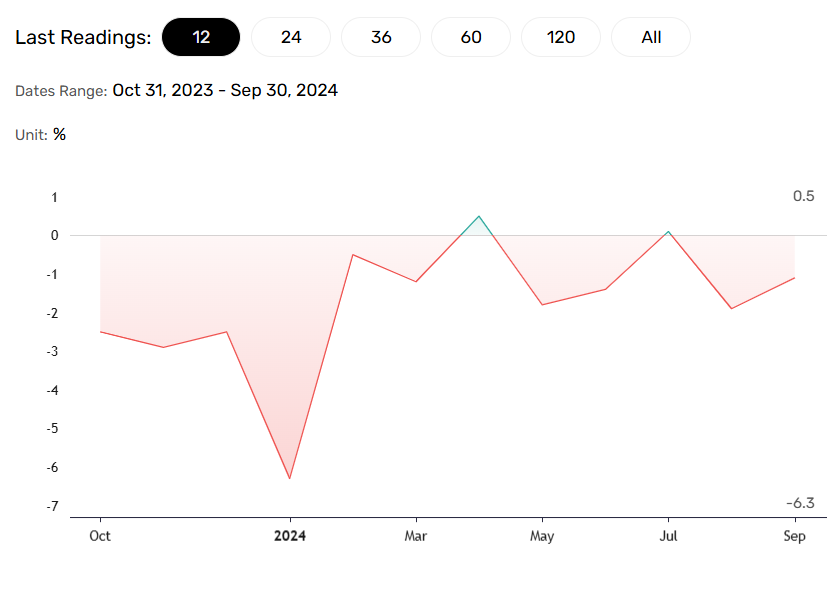

Household Spending and Wage Growth – Crucial Data

On Friday, December 6, household spending and wage growth will be crucial data releases amid speculation about a December rate hike.

Economists expect household spending to fall 2.6% year-on-year in October after declining 1.1% in September. Weaker household spending may dampen demand-driven inflation, potentially delaying the timeline for a BoJ rate hike.

Bank of Japan comments regarding household spending will be important. BoJ Board members have raised concerns about a weaker Japanese Yen pushing import prices, and living costs higher. Support for a rate hike to target living costs could weaken the influence of the household spending data.

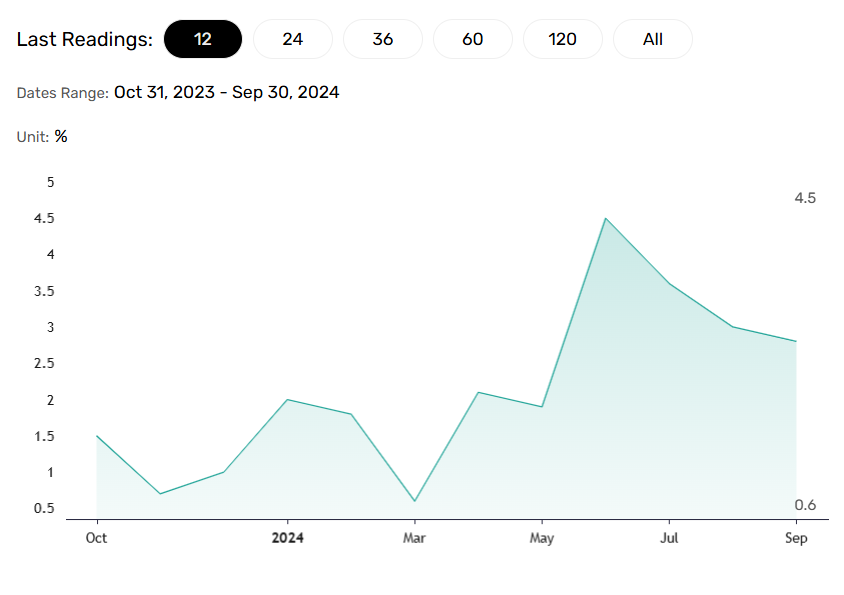

Wage growth will also be crucial. Economists expect average cash earnings to rise 2.6% year-on-year in October, down from 2.8% in September. Softer wage growth may dampen consumer spending and demand-driven inflation, further complicating the BoJ’s decision.

In summary, weaker services sector prices, a pullback in household spending, and softer wage growth may reduce bets on a December BoJ rate hike. Falling bets on a rate hike could drive the USD/JPY pair toward 155. Conversely, higher expectations for a December rate hike could drag the pair below 147.5.

Expert Views on the Bank of Japan Rate Path

Ivory Hill founder Kurt S. Altrichter commented on the Bank of Japan’s rate path, stating,

“The Fed is not the most important central bank to watch right now. The Bank of Japan is. Japanese companies are passing rising labor costs to consumers at the fastest rate in 32 years, supporting the case for a BOJ rate hike.”

Altrichter’s views align with November’s Reuters poll that showed 56% of economists predicting a December hike, up from 49% in the October poll.

US Economic Calendar: Labor Market to Spotlight the Fed

Key US labor market data could influence the Fed rate path, impacting USD/JPY.

The US JOLTs Job Openings Report will draw interest on Tuesday, December 3.

Higher job openings may signal tighter labor market conditions, potentially driving wage growth. Rising wages may fuel consumer spending and demand-driven inflation, potentially pushing a Fed rate cut into Q1 2025.

On Wednesday, the ADP Employment Change data will influence sentiment toward the Fed rate path. Economists expect the ADP to report a 165k increase in employment in November, down from 233k in October.

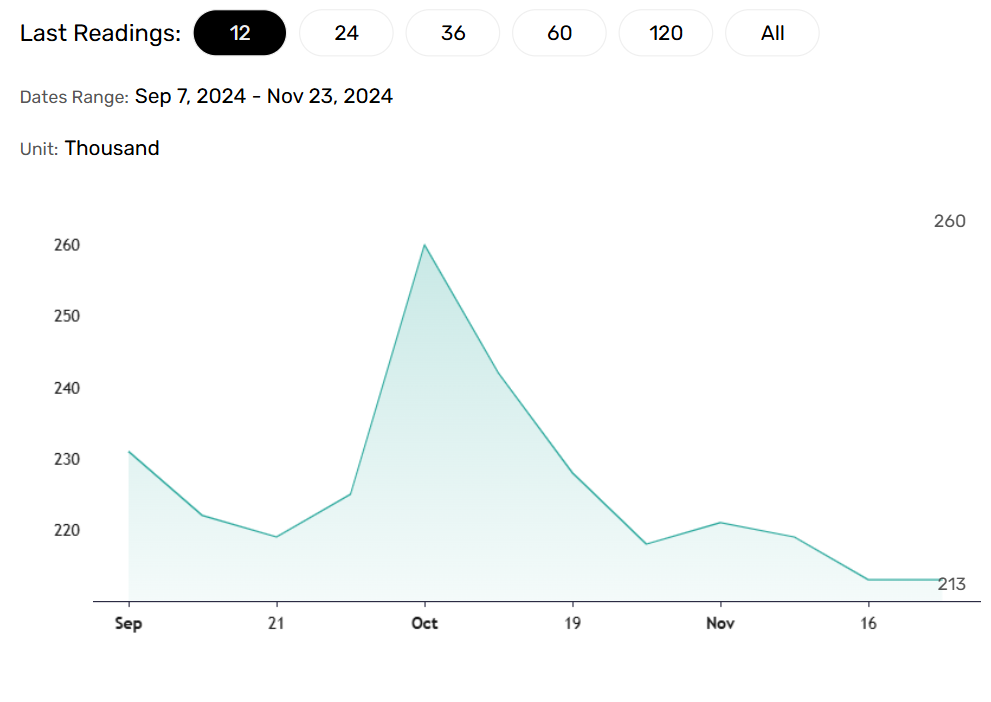

Initial jobless claims, on Thursday, will be another labor market report for investors to consider. Economists predict initial jobless claims to increase from 213k (week ending November 23) to 220k (week ending November 30).

The labor market reports earlier in the week will be a prelude to Friday’s all-important US Jobs Report.

How will the US Jobs Report influence the Fed rate path and the USD/JPY pair?

Friday’s US Jobs Report will be pivotal, with wage growth, nonfarm payrolls, and the US unemployment rate likely to dictate the Fed’s rate path.

Softer wage growth, a sub-100k increase in nonfarm payrolls, and a higher unemployment rate could raise bets on a December rate cut. On the other hand, strong data could temper expectations for a December Fed rate cut.

In summary, rising bets on a December Fed rate cut on weak labor market data could drag the USD/JPY pair below 147.5. Conversely, upbeat labor market data may drive the pair toward 155.

Other US data include finalized private sector PMI and consumer sentiment numbers. However, barring marked revisions, they will likely play second fiddle to the labor market reports.

Short-term Forecast:

Near-term USD/JPY trends will hinge on upcoming Japanese and US data. Monetary policy divergence favoring the Japanese Yen could drive the USD/JPY below 147.5, while falling bets on a Fed rate cut or BoJ rate hike may push the pair toward 155.

Investors should stay alert, monitoring real-time data, central bank views, and expert commentary to adjust trading strategies accordingly. Don’t miss crucial market movements. Follow our real-time FX updates and stay ahead in the markets here!

USD/JPY Price Action

Daily Chart

The USD/JPY sits below the 50-day and 200-day EMAs, sending bearish price signals.

A USD/JPY break above the 200-day EMA could signal a move toward the 50-day EMA and the 151.685 resistance level. A breakout from the 151.685 resistance level may enable the bulls to target the trend line.

Investors should consider the economic indicators and central bank commentary, potentially affecting USD/JPY price trends.

Conversely, a drop below the 148.529 support level could bring the 147.5 level into play. A fall through 147.5 may give the bears a run at the 145.891 support level.

The 14-day RSI at 38.45 suggests a USD/JPY drop below the 148.529 support level before entering oversold territory (RSI< 30).

Dive deeper into the trends. View our latest USD/JPY chart analysis for technical insights.

About the Author

Bob Masonauthor

With over 28 years of experience in the financial industry, Bob has worked with various global rating agencies and multinational banks. Currently he is covering currencies, commodities, alternative asset classes and global equities, focusing mostly on European and Asian markets.

Did you find this article useful?

Latest news and analysis

Advertisement