Advertisement

Advertisement

Bruised UK assets get little respite from grim outlook in Hunt’s budget

By:

By Dhara Ranasinghe LONDON (Reuters) - Finance minister Jeremy Hunt has gone some way towards restoring Britain's market credibility with a predictable budget, but the economy's bleak outlook is likely to keep UK assets at the bottom of investors' lists.

By Dhara Ranasinghe

LONDON (Reuters) – Finance minister Jeremy Hunt has gone some way towards restoring Britain’s market credibility with a predictable budget, but the economy’s bleak outlook is likely to keep UK assets at the bottom of investors’ lists.

Hunt announced a string of tax increases and tighter public spending in a tough plan that was needed after former prime minister Liz Truss’s plan for unfunded tax cuts dealt a blow to the country’s fiscal reputation.

The measures had been broadly flagged in recent days and so investors reacted with relative calm – a sharp contrast to the aftermath of Truss’s Sept. 23 fiscal plan, which sent sterling and British bonds into a tailspin.

But for many investors Thursday’s spending and tax announcements only highlighted what they had long feared – that government borrowing will remain high and the economy weak.

Mark Dowding, chief investment officer at BlueBay Asset Management, said the signal from the Office for Budget Responsibility (OBR), Britain’s independent fiscal watchdog, about a fall in living standards was especially worrying.

“That serves as a reminder of the very tough situation that the UK economy finds itself in,” said Dowding, who helps oversee around $92 billion worth of assets.

“Ostensibly, we’re in a situation where the outlook for inflation is still very concerning and at the same time, the outlook for growth is pretty dire.”

Hunt said the economy was already in recession and announced changes that will mean more people pay basic income tax, with lower threshold for paying the top rate of income tax.

The OBR said freezes on income tax allowances will take the real value of the personal allowance in 2027-28 back to its 2013-14 level.

Dowding said such an outlook could limit the Bank of England’s scope to hike interest rates further, adding that he had extended a short position, or bet, on further weakness in the pound against the dollar earlier on Thursday.

Money market pricing suggested a peak in Bank of England rates of 4.54% by next August, not much changed from before Hunt’s speech.

Sterling was last down around 1% at $1.1782, broadly in line with other major currencies versus a strong dollar. But it has slid almost 13% against the greenback this year, making it one of the worst-performing major currencies.

Britain’s economy shrank in the three months to September at the start of what could be the longest recession in a century. Gross domestic product is now expected to contract by 1.4% next year compared with a projection for growth of 1.8% in the previous outlook published in March by the OBR.

Bond vigilantes

Ratings agency Moody’s said the budget plan restored credibility, but risks remained. A weaker economic outlook and higher borrowing suggested UK government debt will remain consistently above 100% of GDP in coming years, Moody’s said.

Vivek Paul, UK chief investment strategist at the BlackRock Investment Institute, noted that rebuilding credibility comes with economic costs, with Britain now set for a longer recession than the United States or the euro area.

“For years to come, the Treasury will be wary of the bond vigilantes that hastened the demise of Truss and (former Chancellor Kwasi) Kwarteng,” he said.

Hunt had warned in the days ahead of the budget that he could only slow a rise in borrowing costs by showing investors that Britain’s 2.45 trillion pound ($2.91 trillion) debt mountain will start to fall as a share of economic output.

Thursday’s forecasts by the OBR showed that target would be met in the 2027/28 financial year.

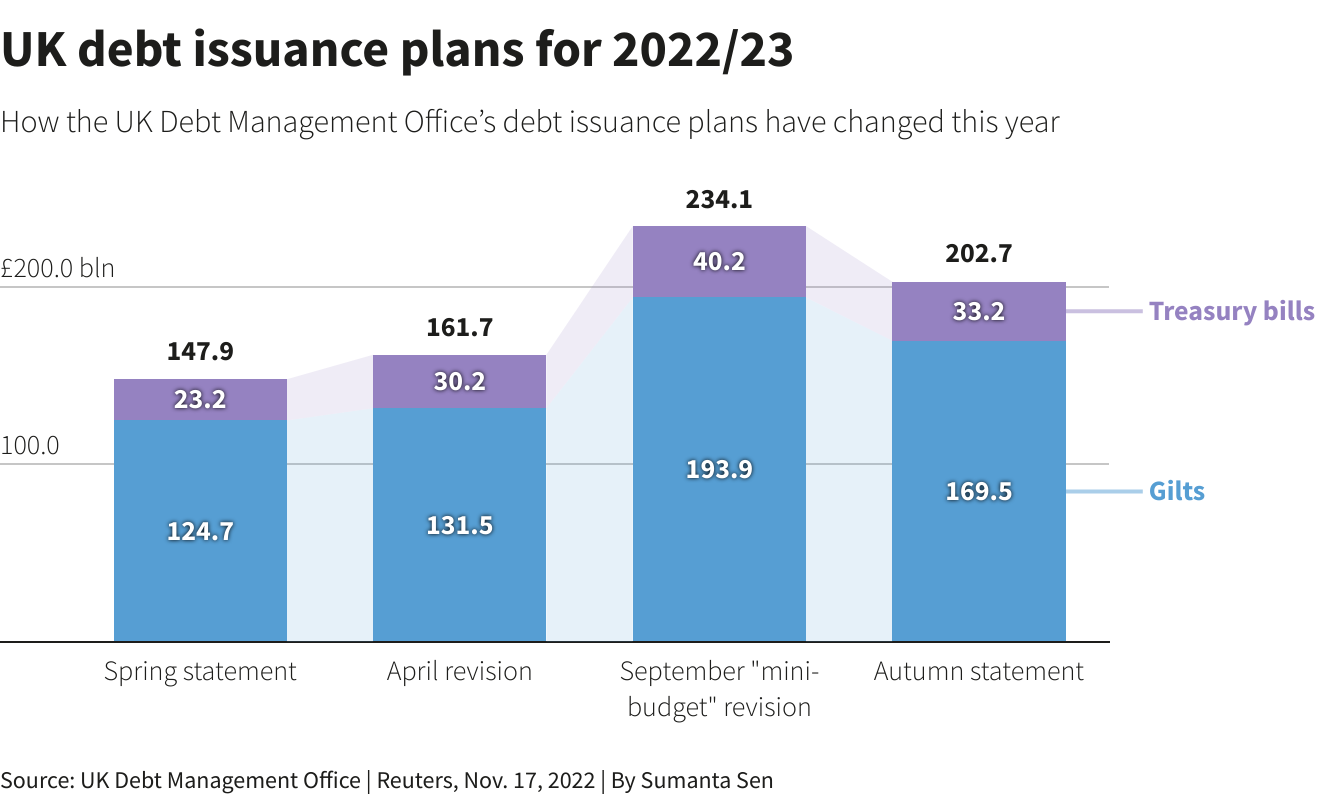

James Lynch, a fixed income investment manager at Aegon Asset Management, said that while gilt sales were expected to fall between now and March 2023, from then onwards, gross issuance would be an “eye-watering” 305.1 billion pounds – 113.8 billion pounds more than predicted in March.

“For the gilt market, that wall of supply is very difficult to price when it is so far in advance and in the short term, the borrowing requirements have been cut. But I would not be surprised that yet again in 2023 we will be talking about the markets ability to absorb a large amount of gilt issuance,” Lynch said.

Britain’s 10-year gilt yield was last up around 7 basis points on the day at around 3.20% – well off a 14-year peak hit in October around 4.6%, but still up over 200 bps this year.

BlackRock’s Paul said his long-term positioning would steer away from gilts, adding that the Investment Institute was keeping an underweight position on UK equities.

“The forthcoming recession – not just in the UK but across Europe as well – makes it tough to make a strong case for UK stock markets, as both domestic and overseas revenue is likely to be under pressure,” he said.

(Reporting by Dhara Ranasinghe, Additional reporting by Harry Roberston, Editing by Elisa Martinuzzi and Catherine Evans)

Related Articles

About the Author

Reuterscontributor

Reuters, the news and media division of Thomson Reuters, is the world’s largest international multimedia news provider reaching more than one billion people every day. Reuters provides trusted business, financial, national, and international news to professionals via Thomson Reuters desktops, the world's media organizations, and directly to consumers at Reuters.com and via Reuters TV. Learn more about Thomson Reuters products:

Latest news and analysis

Advertisement