Advertisement

Advertisement

Column-Crypto regulators may see 10% household exposure as high watermark :Mike Dolan

By:

By Mike Dolan LONDON (Reuters) - Whatever the broader financial or economic stability risks of volatile crypto tokens, government watchdogs may reasonably balk at 10% household exposure to loosely-regulated speculative punts that double or halve in value every 6 months.

By Mike Dolan

LONDON (Reuters) – Whatever the broader financial or economic stability risks of volatile crypto tokens, government watchdogs may reasonably balk at 10% household exposure to loosely-regulated speculative punts that double or halve in value every 6 months.

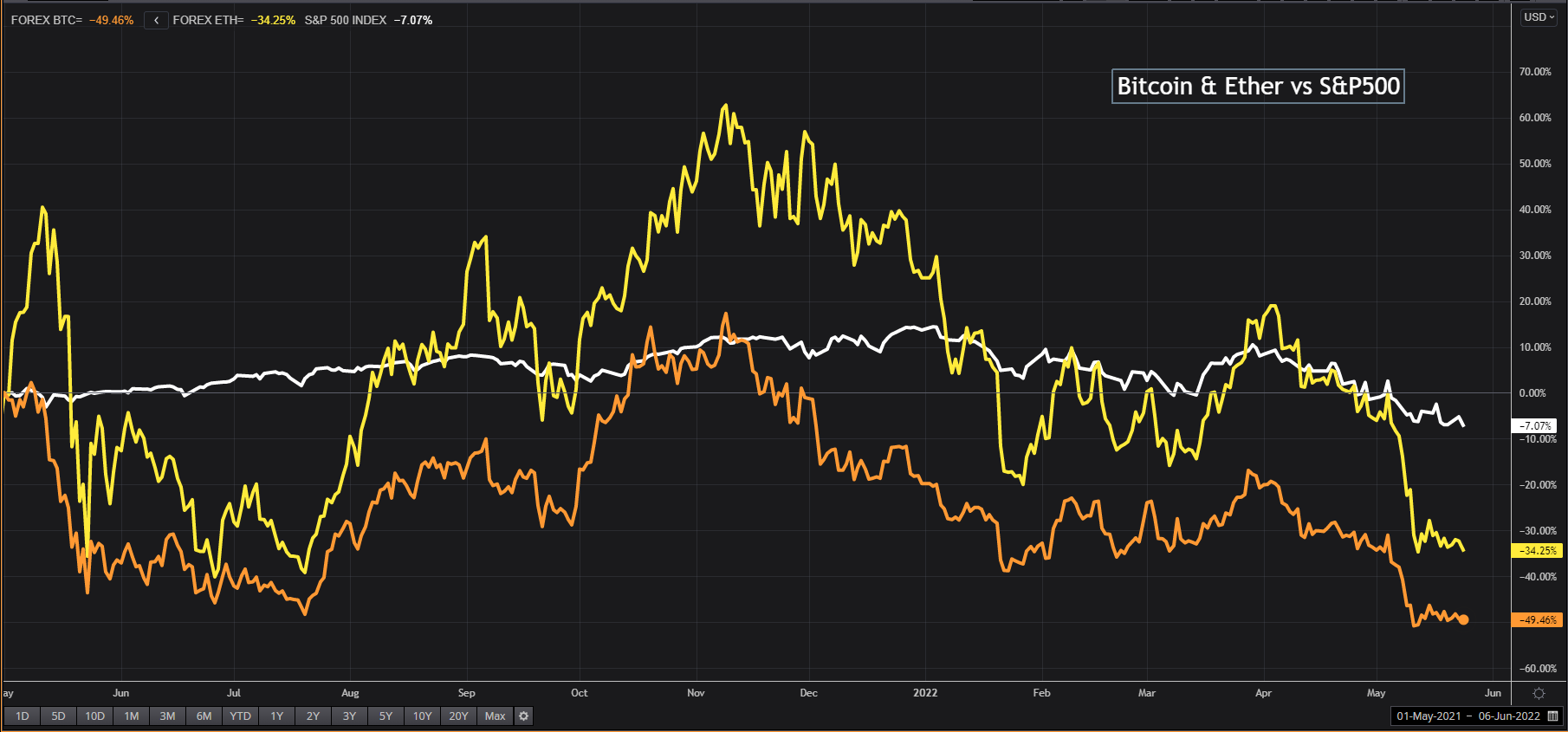

So far this year the leading crypto ‘currencies’ such as Bitcoin and Ether have dropped 40-50% and there’s been an earthquake in the parallel ‘stablecoin’ world of supposedly pegged tokens that act as links from regular finance to the twilight zone of crypto, or ‘decentralised’, finance.

Another typical year in the nether regions of finance? Caveat emptor, some might say.

But the latest twists touched another nerve among governments and central banks who fear they’ve let this ecosystem get out of hand without proper oversight or adequate transparency to reach levels beyond which they may find it difficult to control or shore up.

G7 finance chiefs meeting in Germany late last week cited the crypto turmoil and urged its Financial Stability Board “to advance the swift development and implementation of consistent and comprehensive regulation.”

French central bank chief Francois Villeroy de Galhau reinforced the message this week and upped the urgency at the World Economic Forum in Davos, warning of lax investment protection as well as money laundering risks.

“It’s an emergency question now… I strongly hope we will have this regulation in Europe this year,” Villeroy said.

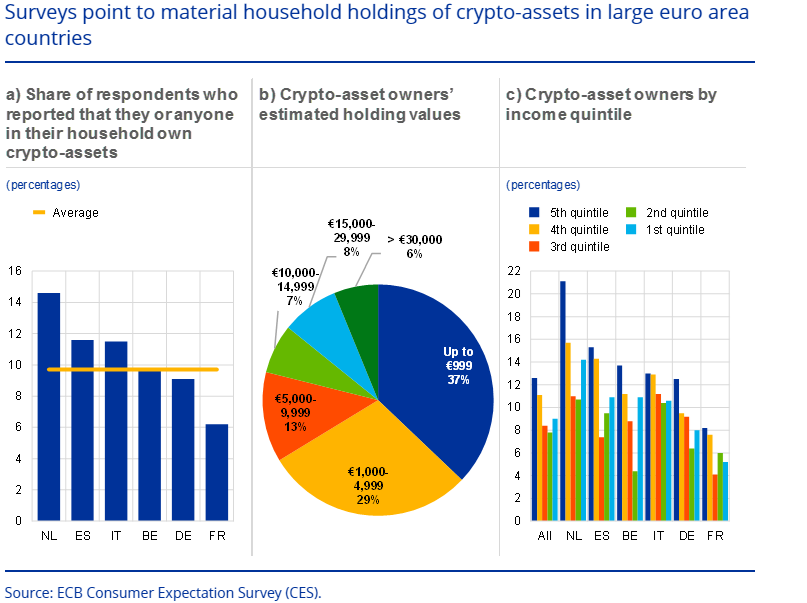

While still relatively small compared to stocks, bonds or real estate, two surveys released this week from the U.S. Federal Reserve and European Central Bank show that at least 10% of all households in both regions have dabbled in crypto as an investment over 2021.

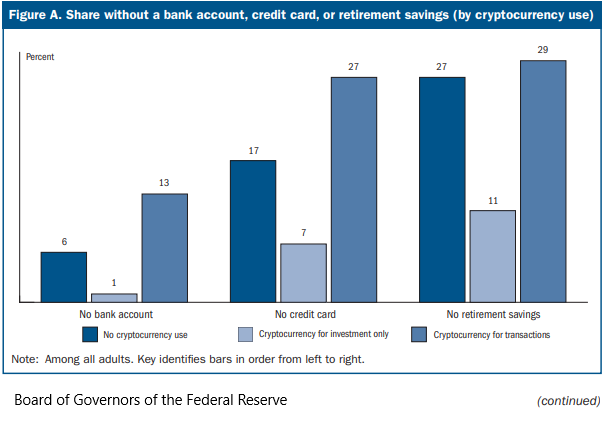

The Fed’s annual “Survey of Household Economics and Decisionmaking” report polled 11,000 adults late last year and painted a relative picture of rude health for consumer finances overall – conducted though it was before one of the worst starts to a year in more than 20 years.

Asking about cryptocurrency for the first time, the survey found 12% of adults used or held cryptocurrency for investment in the previous 12 months. Less than 3% had any reason to use it for payment or remittance purposes.

While this might pale against estimates of just over 50% of U.S. households holding stocks for saving or retirement, it’s likely an uncomfortably large share for governments who see these tokens as having little or no use or value longer term and who fret about financial sharks burning inexperienced savers.

And if, as some estimate, a majority of those holding the tokens arrived over the past year and are underwater at levels over $30,000 or less, then damage limitation may be the first task of watchdogs and governments.

ECB chief Christine Lagarde, for one, said this week that Bitcoin and the hundreds of other lesser-known tokens were basically ‘worth nothing’.

b9febc7a-0299-4725-8764-77a8af66f78e1

cd5d8873-a53f-4833-bd8c-867bdb89c9f52

Worthless?

And for those who think it’s all just a bit of high-octane fun for wealthy folk who can afford to lose some marginal funds in a puff of smoke, there were other sobering details in the Fed survey. While almost half invested in crypto had annual incomes of $100,000 or more, almost a third earned less than $50,000.

The ECB’s Consumer Expectation Survey, meantime, chimed with the Fed findings and showed as many as 10% of euro zone households now own crypto tokens in one shape or form.

Much like the Fed estimate, it showed a “U-shaped” curve in the income quintiles and financial literacy of those invested – concentrated either in richer and highly educated households who could perhaps afford to lose the punt, but also in low income households with low financial literacy scores.

Middle income groups appear to have given the whole thing a bodyswerve.

The question then is whether – much like the marketing of highly speculative and volatile stock or bond funds to retail investors – regulators should finally demand overhaul of rules on marketing, celebrity-endorsed advertising or easy access to these tokens on fintech banking apps or trading portals.

And now may be the time to act while the potential macroeconomic fallout still be limited and before crypto too becomes ‘too big to fail.”

Goldman Sachs estimates the global market for crypto dropped by about a trillion dollars to $1.3 trillion since late last year, with U.S. households exposed to one third of that hit.

Comparing that decline to overall US household net worth of $150 trillion, it saw little additional drag on the wider economy and felt the 20% drop in stocks over the same time would have far more impact.

But for Deutsche Bank analyst Marion Laboure the game is up already. Curbing the speculative excesses of some of the more marginal coins will likely defeat the attraction for many people of being there at all and for those tokens that threaten to rival existing currencies, the hammer will come down harder.

“Many historical examples highlight the power of regulatory bodies to maintain financial stability,” she wrote. “Regulation is coming sooner rather than later.”

Related columns:

COLUMN-‘Mom & pop’ investors left high and dry in tech, crypto meltdown

COLUMN-Crypto warnings invoke U.S. subprime bust, 2008, and all that

(The author is editor-at-large for finance and markets at Reuters News. Any views expressed here are his own.)

(by Mike Dolan, mike.dolan@thomsonreuters.com. Twitter: @reutersMikeD)

About the Author

Reuterscontributor

Reuters, the news and media division of Thomson Reuters, is the world’s largest international multimedia news provider reaching more than one billion people every day. Reuters provides trusted business, financial, national, and international news to professionals via Thomson Reuters desktops, the world's media organizations, and directly to consumers at Reuters.com and via Reuters TV. Learn more about Thomson Reuters products:

Latest news and analysis

Advertisement