Advertisement

Advertisement

Marketmind: RBA set to raise rates, and Powell to the people

By:

By Jamie McGeever (Reuters) - A look at the day ahead in Asian markets from Jamie McGeever.

By Jamie McGeever

(Reuters) – A look at the day ahead in Asian markets from Jamie McGeever.

The show goes on. Just.

World and Asian stocks crept higher on Monday despite an increase in U.S. and global bond yields, and ahead of an expected interest rate hike in Australia and hawkish remarks from Federal Reserve Chair Jerome Powell on Tuesday.

On top of the Reserve Bank of Australia (RBA) rate decision on Tuesday, investors in Asia have a slew of potentially market-moving indicators on the docket, including Chinese trade and FX reserves, South Korean GDP and inflation from the Philippines, Thailand and Taiwan.

Investors are going into these events in a fairly upbeat mood. MSCI’s World equity index rose for a third straight session on Monday, its best run in a month, and the Dow Jones rose for a fourth day, its best run in two months.

The gains were minimal, but they came despite a rise in global bond yields on Monday and significant event risk on Tuesday.

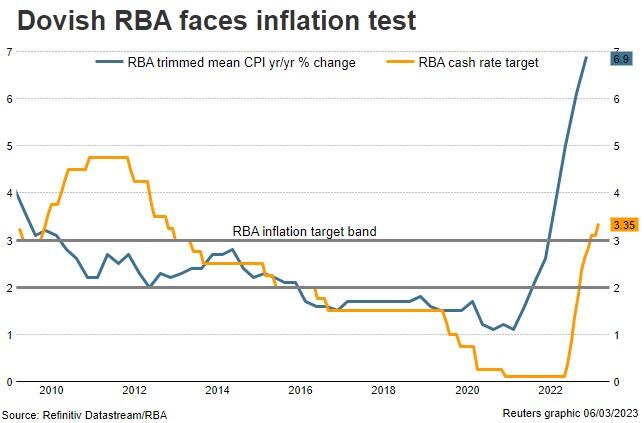

Arguably the main event in Asia will be the expected quarter point rate hike from the RBA, which would take the cash rate up to 3.60%.

Analysts expect one more 25 basis point increase in the second quarter of the year, leaving the cash rate at 3.85%, its highest since 2012. If policymakers are to err on one side or the other, it will likely be on the hawkish side.

That would be in line with the RBA’s signaling last month and with rate-setters at other major central banks – Austrian central bank chief Robert Holzmann, a hawkish member of the European Central Bank’s (ECB) governing council, told German business daily Handelsblatt that the ECB should hike rates by 50 basis points at its March, May, June and July meetings.

Tuesday’s focus rests squarely on the first of two Congressional appearances this week from Powell. Rates and bond market pricing suggests traders expect him to deliver hawkish testimony to lawmakers – the implied terminal rate is holding around 5.50% and traders are a putting near one-in-three chance of a half-point rate hike this month.

Again, the question is: how long can equity markets hold up and volatility stay depressed, if yields and Fed expectations continue to grind higher?

On the Asian data front, China’s FX reserves for February could cast a light on whether Beijing is starting to reduce its huge holdings of dollar-denominated assets amid the sharp rise in U.S.-Chinese tensions.

Analysts expect a decline in reserves to $3.16 trillion from $3.184 trillion in January, which would be the first monthly fall since September.

The latest valuation-adjusted figures show that China sold Treasuries last year, but bought a similar amount of U.S. agency debt, thereby keeping its exposure to dollar assets broadly steady.

Here are three key developments that could provide more direction to markets on Tuesday:

– Australia rate decision (consensus: +25 bps to 3.60%)

– China trade, FX reserves data (February)

– U.S. Fed Chair Jerome Powell’s semi-annual monetary policy testimony to the Senate

(By Jamie McGeever; Editing by Josie Kao)

About the Author

Reuterscontributor

Reuters, the news and media division of Thomson Reuters, is the world’s largest international multimedia news provider reaching more than one billion people every day. Reuters provides trusted business, financial, national, and international news to professionals via Thomson Reuters desktops, the world's media organizations, and directly to consumers at Reuters.com and via Reuters TV. Learn more about Thomson Reuters products:

Did you find this article useful?

Latest news and analysis

Advertisement