Advertisement

Advertisement

Column-Hedge funds to Fed: you win: McGeever

By:

By Jamie McGeever ORLANDO, Fla. (Reuters) - Hedge funds have significantly increased their record bet on higher short-dated U.S. bond yields, confirming that whatever fight they had put up for an imminent Fed pivot on rates, it is well and truly over.

By Jamie McGeever

ORLANDO, Fla. (Reuters) – Hedge funds have significantly increased their record bet on higher short-dated U.S. bond yields, confirming that whatever fight they had put up for an imminent Fed pivot on rates, it is well and truly over.

Funds’ historic short position in two-year Treasuries futures coincides with the recent ramping up in anti-inflation rhetoric from Fed policymakers, including those of a more dovish inclination, such as San Francisco Fed President Mary Daly.

Financial markets are giving up hope that the Fed will take its foot off the rate-hike pedal any time soon. Hedge funds, going by Commodity Futures Trading Commission positioning data, have thrown in the towel completely.

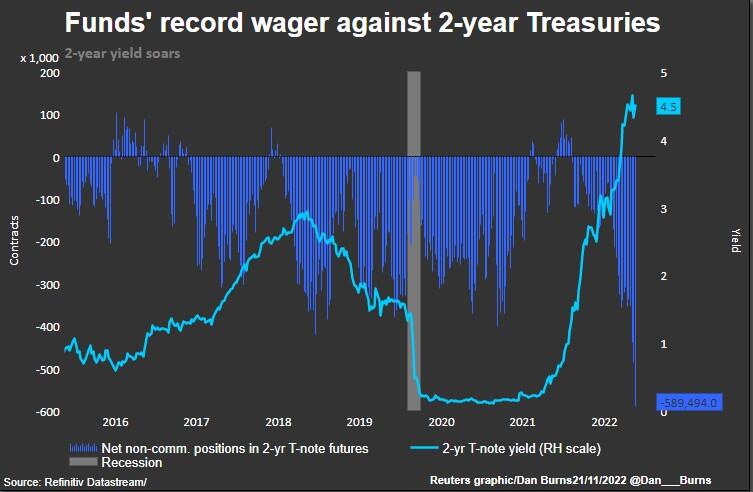

The latest CFTC report shows that speculators increased their net short position in two-year Treasuries futures in the week to Nov. 15 by more than 100,000 contracts to a fresh record net short position of almost 590,000 contracts.

The pace of the move has really accelerated lately – the total net short has almost doubled in just six weeks and has swollen by almost 240,000 contracts this month, putting November on course to be the second most bearish month since these contracts were launched in 1990.

A short position is essentially a wager that an asset’s price will fall, and a long position is a bet it will rise. In bonds and rates, yields fall when prices rise, and move up when prices fall.

Hedge funds take positions in short-dated U.S. rates and bonds futures for hedging purposes, so the CFTC data is not reflective of purely directional bets. But it is a pretty good guide.

Treasury yields have fallen in the last couple of weeks – the 2-year yield tumbled around 50 basis points from a 15-year high of 4.80% – as the latest readings of inflation have come in well below expectations.

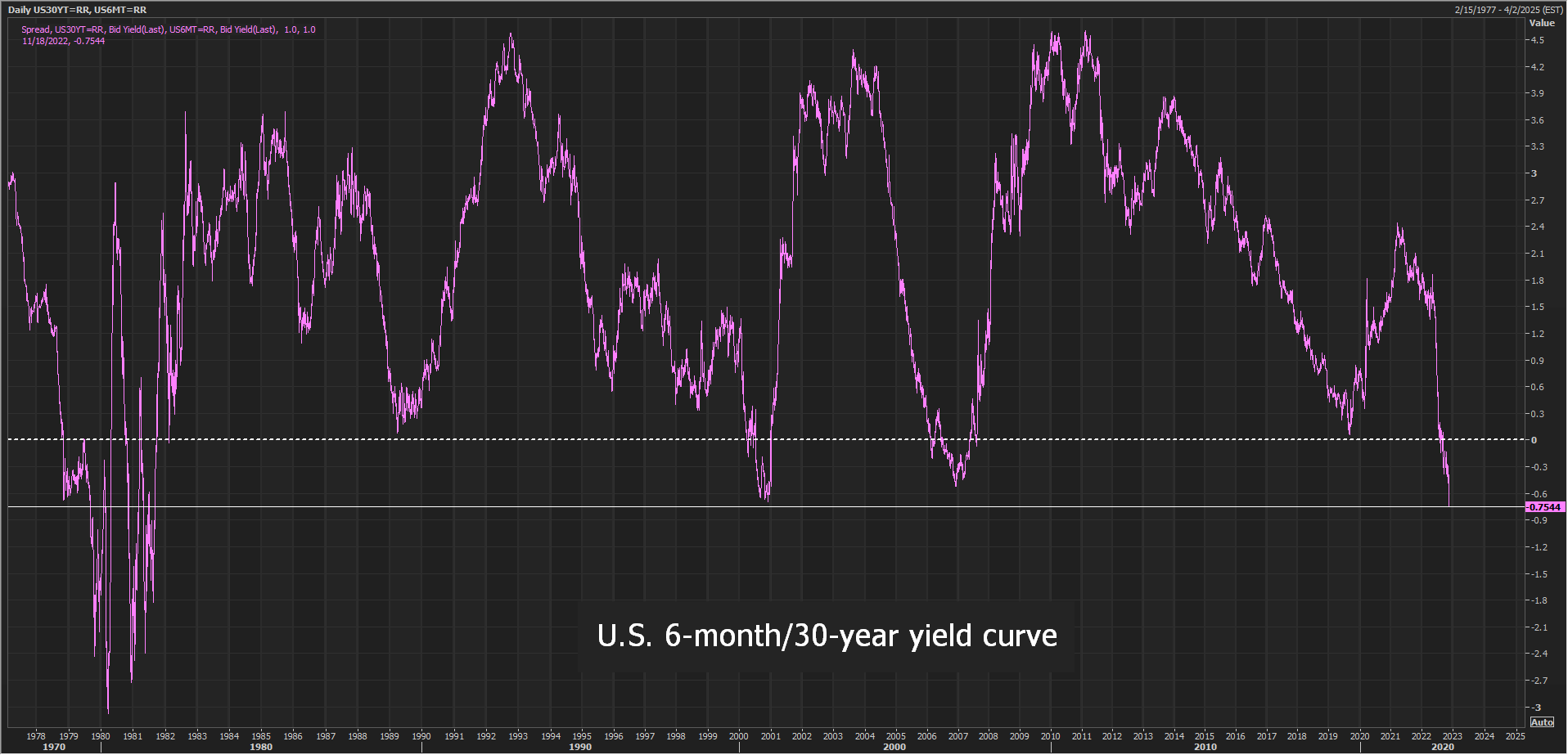

But short-dated yields have held up much more than long-dated ones. Fed officials have made clear they will not get complacent, the implied terminal rate for next year is back above 5%, and yield curves are inverting across the maturity spectrum.

The 2s/10s curve is its most inverted since 2000, and the last time six-month T-bills yielded this much more than 30-year bonds was 40 years ago.

History shows that an inverted 2s/10s yield curve – when two-year borrowing costs are higher than 10-year rates – almost always precedes recession. Funds’ record short position in two-year Treasuries futures suggests that’s exactly what speculators are positioning for again.

(The opinions expressed here are those of the author, a columnist for Reuters.)

Related columns:

– Fed may harangue markets to prevent premature pivot

– Fed ‘pivot’ draws closer, but the word has had its day

– Fed may be alert to favoured yield curve alarm

(By Jamie McGeever; Editing by Clarence Fernandez)

About the Author

Reuterscontributor

Reuters, the news and media division of Thomson Reuters, is the world’s largest international multimedia news provider reaching more than one billion people every day. Reuters provides trusted business, financial, national, and international news to professionals via Thomson Reuters desktops, the world's media organizations, and directly to consumers at Reuters.com and via Reuters TV. Learn more about Thomson Reuters products:

Latest news and analysis

Advertisement